It’s no secret that one of the top stories in today’s real estate market is low housing supply and high buyer demand. If you’re a first-time buyer looking for a starter home or are someone who’s interested in downsizing, it may be worth considering a condominium (condo) as a worthwhile option.

In fact, trends indicate condos are gaining popularity among buyers. In the latest Existing Homes Sales Report from the National Association of Realtors (NAR), the data shows condo sales rising throughout the first half of this year (see graph below): There are a few reasons more and more people are opting to buy condos – the benefits of condo life can be quite compelling. Let’s explore the main perks to find out if a condo is a good fit for you.

There are a few reasons more and more people are opting to buy condos – the benefits of condo life can be quite compelling. Let’s explore the main perks to find out if a condo is a good fit for you.

Affordability

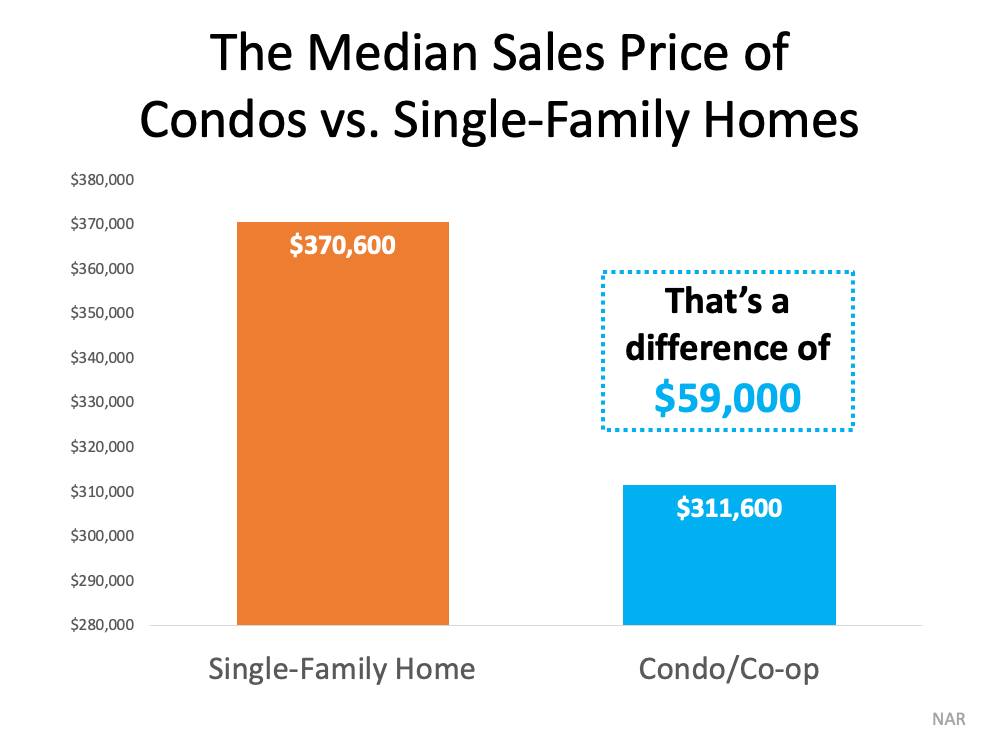

According to the NAR report, the median sales price of a condo is roughly $59,000 less than the median price of a single-family detached home (see graph below). This makes condos a great option for first-time homebuyers, those with limited down payment savings, or those looking to save money by downsizing.

Maintenance

A recent article from BankRate adds low maintenance as another perk of a condo lifestyle. Generally, exterior maintenance for condos is handled by a Homeowner’s Association (HOA). This can include things like landscaping and upholding a certain standard of cleanliness and condition for walkways, siding, and roofs. If you’re looking for a lower-maintenance option or see the appeal in being hands-off with upkeep, condos may be a good choice for you. With exterior maintenance off your plate, you’ll have more time for yourself and your hobbies.

Amenities

You can use that free time to enjoy some of the value-adding features your condo community may have, which could include dog parks, pools, a rentable clubhouse and grilling area for events, and more. If being able to host or attend community social outings is important to you, condos may give you more opportunities to enjoy the company of your neighbors. As a bonus, some condos even have gyms and on-site security teams.

Ultimately, the choice is yours. Condos are great options that often come with various features and benefits that may be important for your lifestyle. Fannie Mae sums up the appeal nicely:

“Condominiums, or condos, can be great alternatives to detached homes. City dwellers, singles, couples, seniors, and many others may find condos that suit their needs and budgets. Others may simply prefer low-maintenance living. Buyers who feel ‘priced out’ of homes may discover condos offer an affordable homeownership alternative.”

Bottom Line

If you’re looking for a home, it may be time to consider a condo as an option. Let’s connect to explore if one would be a good fit for your homeownership needs.

![Waiting To Buy a Home Could Cost You [INFOGRAPHIC] | Simplifying The Market](https://files.simplifyingthemarket.com/wp-content/uploads/2021/07/29150309/20210730-KCM-Share-549x300.png)

![Waiting To Buy a Home Could Cost You [INFOGRAPHIC] | Simplifying The Market](https://files.simplifyingthemarket.com/wp-content/uploads/2021/07/29150304/20210723-MEM-1.png)

![Experts Agree: Options Are Improving for Buyers [INFOGRAPHIC] | Simplifying The Market](https://files.simplifyingthemarket.com/wp-content/uploads/2021/07/15150310/20210716-KCM-Share-549x300.png)

![Experts Agree: Options Are Improving for Buyers [INFOGRAPHIC] | Simplifying The Market](https://files.simplifyingthemarket.com/wp-content/uploads/2021/07/15150312/20210716-MEM.png)